Dear readers,

I have moved to Substack and I will be writing here from now on:

👉 andrewchen.substack.com

In the meantime, I will leave andrewchen.com up for posterity. Enjoy!

(Above: No, it doesn’t really look like this — and yes it’s mostly office parks and tech billboards. But I like to pretend)

You’ll never regret spending time in SF

If you work in tech, you’ll never regret spending 3-5 years in the Bay Area. This is advice I’ve been giving to people for years, and it’s shaped by my own experience — after all, I moved to the Bay Area in 2007 and it completely changed my life.

How?

I met tons of incredible people, some of whom went on to create major products and found unicorn companies. Most are still building

I was introduced to many investors who today run some of the major VC firms and investor networks

learned so much!

made life long friends

formed fundamental aspects of my world view

Because of the recent AI boom, I’ve been meeting a lot of folks who are new to SF. Many folks very intentionally want to build out their network and get rooted in the Bay Area, and to fully immerse themselves in tech. I learned so much in my first few years and wanted to pass along some of my lessons.

In particular:

personal viral loop: Asking people for more people

ask for advice and listen

why it’s helpful to “have a thing”

know what you bring to the table

find your cult

how blogging/tweeting is helpful

why I avoid conferences/events

building a network while you sleep

Getting started by asking for intros

I first moved to the Bay Area as a 25 year old nerd with a light resume and big tech dreams. I knew exactly 2 people, and that was it. But very intentionally, I wanted to build a strong professional network and to learn from people. The first thing I did was to be intentional and methodical about it, by asking the two people I knew to please sit down and suggest 5 to 10 people for me to meet — an they did a number of email intros for me. The amazing thing about SF tech culture was that this worked! Although the intros were very light on context, people were willing to grab coffee and share what they were working on, and what they’ve learned over the last couple years.

After each meeting, I would follow up with a few bullet points on what I learned from the conversation, and then ask for two or three more people to meet. This was like building my own personal viral loop, where every chat turned into a few more chats. For my first six months in the Bay Area, I ended up meeting 3 to 5 new people every day. I learned an incredible amount. I can confirm this is still possible, as others I know have done it in recent years.

How to add to each convo

You might ask, what do you end up talking about? What value can you add as someone who’s just moved to the area and is starting in tech? The answer is, you simply ask for advice. People move to the Bay Area from all over the world because they’re incredibly passionate about what they’re building. They love talking about that. and if you have something that you’re passionate about too, and ask for advice, you were sure to get a lot of it. The culture in the SF tech community is very open and the intro culture makes it easy to chat with a variety of new people.

For me, I was coming from Seattle, and I asked people about various mysteries of the tech industry I didn’t understand as an outsider. Why were there so many consumer successes in the Bay Area but not elsewhere? How does angel investing and VC work? Why don’t they build more houses/offices in the Peninsula? And so on.

Having a “thing”

That said, the conversations are more productive when you have “a thing.” What I mean by that is that all of these conversations and networking are more useful when you are starting a company, creating a new podcast, are working on a new project or book, or something else. When you have a directed goal in mind, then the conversations often are more valuable for all parties involved, because you were making yourself an expert in a particular area and your questions are more relevant. Otherwise you will surely encounter very busy people who simply refuse to “grab coffee” to “catch up” because it’s a poor use of time. I encourage you to be on a quest of your own, and even better a particularly interesting quest, so that your conversations with people can be as productive as possible.

In my case, I was very interested in the state of the art on growing users, metrics, network effects, and marketing. I asked everyone about this topic, and began to develop my own ideas that I would share freely. Eventually, it became clear that a few small communities orienting the PayPal mafia were the furthest along in their thinking. And that’s how I ended up being exposed first to concepts like retention curves, DAU/MAU, viral loops, and so on.

These ideas were interest to me, because my professional experience leading up to that point was actually an adtech. I had previously worked in online ads, with customers from WSJ, CBS, MySpace, etc, and had even gotten a patent filed on ad targeting (yes, US7747676B1). I had a superpower in my domain knowledge of CAC, A/B testing, funnel optimization, lead gen, etc, and began to merge all of this thinking with consumer products. In 2007 this was cutting edge at a time when product success was often measured by vanity metrics such as the total registrations for a product. This bit of specialized knowledge was what I brought to the table, and I talked about some of those learnings and ideas, and how they might apply to products. Sometimes I’d get intros to interesting people simply because of this expertise, which I appreciated.

Find your cult

I sometimes joke that the Bay Area is ruled by cults. Back in 2007, there was a cult surrounding quantified self, which intersected with lots of folks kicking off Crossfit, keto, Soylent, and other health trends. There were people building robots and hardware. The PayPal mafia was a thing, but look a little closer, and there was a huge network of Stanford CS people and even Canadian mafias. And Burning Man people. In 2007, YCombinator was just getting off the ground, and I was lucky to meet many of the early folks back when they were living in North Beach on strictly ramen diets. Today, those cults have evolved but they still exist — there is a huge advantage in finding one that suits you, or even better, starting one. Years later I joined Uber and had the idea one day there would be an ex-Uber cult. I think that’s happened, and there’s been countless founders, investors, and builders from that network.

Why blogging/writing is so helpful

In the first year, I learned the importance of writing things down. The other thing I started to do right away was to write down everything that I was learning. I started a real/professional blog at the beginning of 2007 on the Blogger platform and initially, I got writers block because I was trying to come up with amazing and grandiose ideas that I would share with the world. My first month, I had 20 email subscribers, from friends and family I forcibly subscribed.

But eventually, I created a more successful strategy for myself, where I would simply document what I was learning. It turned out that if one person told you a unique idea I would treat it like it was a secret (or at least, I would ask permission). It was often the case that a dozen people would talk about the same idea, and there was simply consensus memes floating around in the ether, and I focused on writing those down. I find that a lot of my blogging has been less about inventing brand new ideas, but instead simply collecting and expanding on the current tech zeitgeist. A few months in, Robert Scoble linked to my blog from his, and that helped a ton. (Thank you!)

It was with this attitude that I began to write about viral loops, growth, hacking, measuring retention, and product/market fit, and all the other concepts that came to defined my writing.

There is a virtuous cycle in talking to interesting people, writing down expanded versions of ideas that come up, thus being exposed, to more interesting people, and rinsing and repeating. This core loop helped power the growth of my professional network over the first few years. In later years, I added a dash of advising and investing.

15+ years later it’s weird to think that accidentally developing a habit of writing and blocking would still be with me today. In fact, this habit is so powerful that I recommend doing it above and beyond almost any other professional “networking” activity. Of course today you might be making videos or podcasts instead of writing. Or if you’re an engineer, publishing your code on GitHub. It’s all the same concept. Putting your work into the world, whether it’s text or video or code, and letting that engage the world.

In this way, you are building your network while you sleep. People find you and your work and your ideas, so that you don’t have to put in time for 1 million coffee meetings.

Why I avoid conferences

And in particular, I find writing to be much more powerful than going to conferences. One thing you’ll notice about the SF tech industry is that there are endless events and conferences. Whereas a secondary startup hub might have a major tech event once every month or two, SF has them every day. There’s office warmings, product launches, new AI meetups, hangouts at Dolores, big splashy conferences, hackathons, and so on. There are endless varieties.

Build a network while you sleep

However over time, I’ve found them to be less scalable than writing. They are fun, and it’s much easier to have a one on one conversation than it is to create a content. When you really think through how much time you spend getting to a conference, all the time between sessions, and when you speak how few people are actually in the audience listening. Contrast to any kind of digital platform where you can write a blurb and 1000s of people see your ideas.

Going back to my original assertion, I think it is hard to regret 3-5 years working in SF. Many people say it’s not a great place to live — and sometimes that seems true. Other folks hate the monoculture. However you can always move home, and when you do, you’ll always be the person with Silicon Valley tech experience. And furthermore, the learning curve is so strong, particularly for startup founders, as is the network of capital and peers. It’s a one of a kind place, and I highly recommend founders spend a few years even if they don’t intend to stay in the long run.

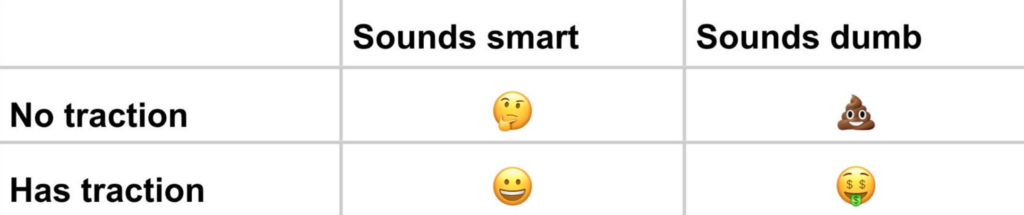

The “Dinner Party Jerk” test is a solution to a common problem:

Startups often struggle at pitching their team, even though for the earliest stage companies, it’s incredibly important to do it well to raise capital — as I’ve described it below:

Pre-seed- Bet on the team

Seed- Bet on the product

Series A- Bet on the traction

Series B- Bet on the revenue

Series C- Bet on the unit economics

To figure out if you are properly pitching yourself in your team, run the thought experiment of describing yourselves at a dinner party. If you are pitching yourself hard, then if you are a kind human, you will turn red and blush with wild embarrassment. The reason is that a proper pitch includes many of your credentials, your achievements, the ways in which you and your team are highly unique, and we simply don’t talk like this at dinner parties. And yet this is exactly what you should do when you talk to investors, partners, customers, and potential employees.

A few years back, a big group of Nordic founders came by Silicon Valley. When I asked them their biggest learning on the trip so far, they said- We have to learn how to pitch our startup in the “American” way More self promotional, emphasizing the future not the past, talking about what it could be not what it is, playing up even small bits of proof points, etc. Describing usage and telling stories, not just revenue. They told me the investors back home didn’t care for this style.

Don’t hold back

Be the dinner party jerk, pitch yourself hard. Don’t hold back. Your shyness and cordiality is not helping.

I find that most founders tend to focus, primarily on describing their idea to the exclusion of everything else. I’ve heard thousands of “elevator pitches” and they generally focus on the idea and not the team, the market, differentiation, or anything else. And they downplay their achievements or omit them.

Of course what you emphasize depends on your background. It’s often described that there are repeat founders and first time founders, but furthermore, there’s another axis, which is about obvious credentialing versus not. For first time founders that are starting a gaming company, for instance, but have already spent years at a top company in the field, a quick modification to the elevator pitch, mentioning that, is both beneficial and quite obvious. But what do you do, you’re an uncredentialed first time founder?

Then the question becomes, what is your “earned secret“ behind the idea? Having a pithy story about how you were a Shopify seller, and that’s how you got to building any commerce product, is incredibly helpful. And if you have some metrics or an observation about the market that’s non-obvious, showing your expertise in the field, is even more valuable. If you have various credentials either professional, or academic or open source, achievements, it might be worth working those in even if not directly related.

The other very awkward thing is to use facts and figures to describe yourself. If in your previous work, you worked on an app that served millions of people, or for your current company, you recently launched and got your first 10,000 users, you should save these numbers. Any traction and any validation is incredibly helpful proving your case. And of course, this is another thing that would make you a dinner party jerk.

Why don’t we do a better job of this? The dangers of conformity

You might be going through a moment of introspection now and asking why am I like this? Why do I downplay achievements when I should be amping them up?

My answer to this, is conformity. In real life, we often subconsciously conform to the people around us. If you go off at a friendly gathering about all the cool stuff you’ve done, and why you’re going to be great, there’s a fear that you’re exaggerating the differences between yourself and others. There’s a fun theory from evolutionary psychology that shyness is an evolved trait to keep us safe in a world where we grew up and tribes of a few hundred people, and a few wrong words might follow us around for our lifetimes.

This is also my theory for why people are reluctant to engage on social media and share their knowledge, when it’s obvious that it might be very helpful to them professionally.

TLDR; there’s pitch mode and dinner party mode. Learn to turn the former mode on!

Be an optimist

You have to be an optimist about your own product, your own startup, and yourself. That’s why when you pitch — whether to investors, to prospective employees, or partners, it’s important to talk about what might happen, not what you are doing today.

There’s a whole style to this type of pitch, and it’s a futuristic point of view that leans into optimism:

Emphasize the future, not the past

What it could be not what it is

Play up even small bits of proof points

The big things that might happen, if it works

The upside rather than risks

Signs the customers love the product, rather than revenue metrics

Why this team has the grit and special knowledge to do it, not the credentials and work experience

A unique narrative about why the world is moving this way

Why you’re starting with a wedge, but your ultimate market is huge

I previously referenced the idea that international founders often describe this as the “American” way of pitching — the funny thing about this is that this isn’t the “American” way of pitching, it’s actually specific to the Bay Area tech ecosystem. It’s incredibly optimistic and futuristic that founders choose to describe their startups in this way, and furthermore, the people who hear these pitches choose to believe them.

Why this is the only way to pitch to investors, employees, and partners

Let me also make the argument that this is the only logical way to convince people to join you on your journey.

1. Investors

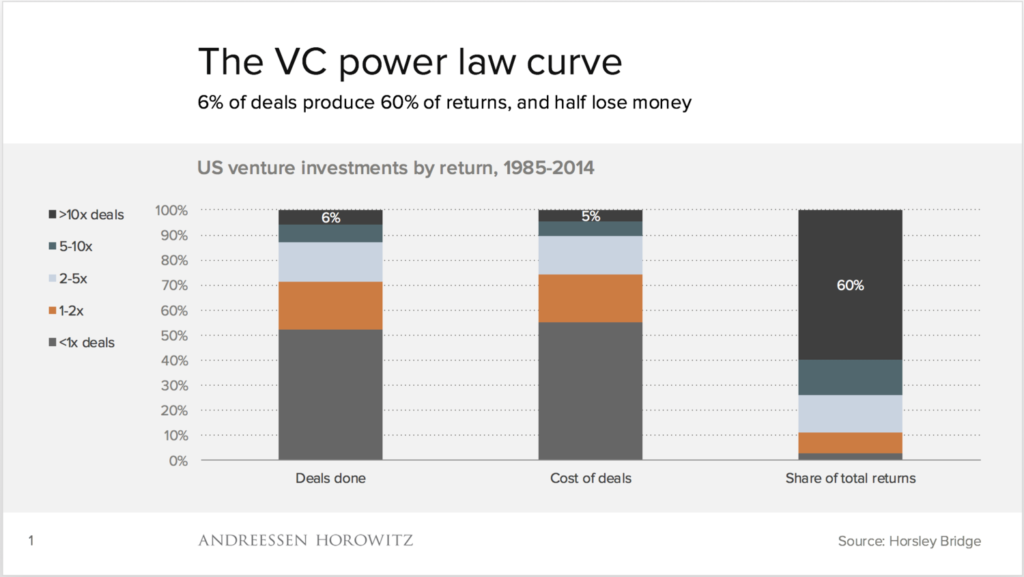

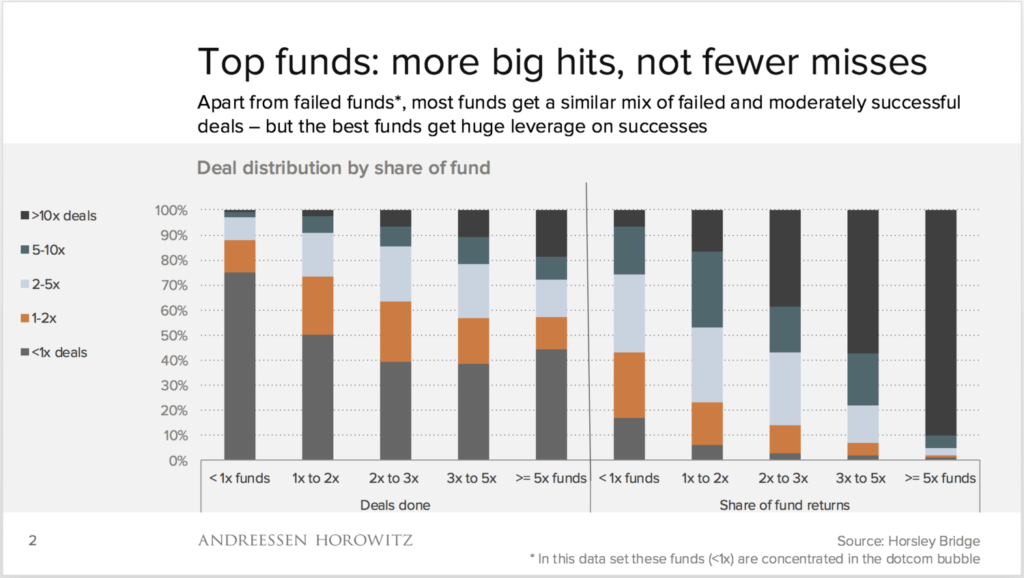

First, let’s talk about startup investors. a portfolio of startup investments is inherently risky, and the physics of venture math means that the winners have to be really big. It’s commonly said that out of a portfolio of ten companies, generally about half the investments will go to zero, three will return a little bit of money, and that the top one or two will return 10x plus and make the fund work. As a result, professional venture investors are trying to understand if you have what it takes to be one of those top two, and if you don’t if you’ll die trying. A lot of this assessment focused on the market or your numbers, but sometimes the real question is about your ambition.

So they are trying to answer a simple question: Do you WANT to create one of the leading companies in the industry?

Focusing on the future and on the upside shows your will to power. It allows investors to gain a sense of that signal. If you’re focused too early on profitability, rather than growth, or retaining your piece of the pie, as opposed to growing the pie as large as possible, that’s an important signal. The point of this isn’t to mislead investors into thinking that you’re trying to do something that you’re not, but rather, if you are shooting for something big, you have to really express that in the clearest way possible.

The perspective is often directly reflected (and not) in the slide decks I review at a16z. Does the product slide describe the features of what the app has today, or does it talk about the product roadmap of what’s going to be built in the future? Do they user projections or financial forecasts simply show the last year’s performance, or does it tell a story about how the business is about to inflect? Oftentimes when founders are too conservative about their story it’s hard for investors to understand what they’re trying to do in the long run. Instead, I love it when founders tell the big story. Of course I’m going to discount it and round down, and assume that many features are never shipped. But I love to see it.

2. Employees

Second, let’s talk about employees. typically when you’re hiring your first few employees, you might be able to give out a few percentage points each, particularly for key people (like engineers or designers). but within a few hires, you end up needing to convince people to work for below pay, and for a fraction of a percent of the company. Why would they do this? Why would they work for you instead of either starting their own company or getting a cushy gig somewhere else where they might be paid much more?

The asymmetric advantage of startups compared to many other opportunities, is that they are adventurous and fun. The startup might fail, but the work is generally a lot more interesting than what you can do elsewhere. The responsibility and scope that a junior employee might have might go way beyond what makes sense at any other company.

And of course financially there is upside. For founders to convince high-quality employees to join their outfit, it’s often important to lean into a sense of adventure. What’s more adventurous than tackling a big huge goal, that might not work, but if it works, it’s going to be amazing? For founders to communicate the sense of adventure, they need to be able to weave a narrative. Maybe it’s us versus them, or David and Goliath. Perhaps it’s exploring the unknown, and going to the frontier when no one else is there. If you can’t tell the stories, how can you expect people to follow you? Thus I find it important to tell the futuristic narrative that’s ambitious, full of surprises and upside, and has a possibility of failure too. It makes the work meaningful and makes the potential economic upside worth something.

3. Journalists, partners, and more

We’ve talked about investors and employees, but there’s actually a long tail of many other constituents that benefit from a futuristic outlook. if you’re talking to journalists and pundits, you have to compete with thousands of other companies that they’re going to meet this year, and you have to catch their attention. If you’re marketing, an event at a conference adjacent to dozens of other events, you have to catch the eye of attendees. An optimistic, futuristic perspective gives you room to tell the story about the problem you’re trying to solve, and why your startup will be incredibly important once you get there.

You might say that the world is full of cynics. Perhaps you are from a region or an industry where most people nitpick all the reasons why fail. Maybe they want you to focus on minimizing downside risks, or acknowledging your potential problems, and won’t treat you as credible unless you do. If that’s your industry network or your social network, I urge to you to escape. Seek out those who share your optimism, and the same values and beliefs about the future. it’s one of the reasons why the Bay Area has been such a powerhouse over the last few decades. Yes, there’s knowledge and investors here, but more important is the culture.

The last point I make is about yourself. You should talk about what you’re working on in an optimistic way to help create meaning for yourself. For those of us who grew up in a generation that adored Steve Jobs, there’s always been the goal to put a dent in the universe rather than to sell sugar water. Thinking about the future, and the upside of what you might be able to create, is a great way to give meaning to the nights and blood and tears that we put into our work. If you’re simply working on a new product only because it’s a good money-making opportunity, I guarantee that your sense of meaning will fade when times get tough. You’ll ask yourself, why am I doing this? If you don’t have a Northstar to guide you on an inevitably rocky, entrepreneurial journey, you’ll inevitably get lost. That’s when the FAANG job will seem really appealing.

Obviously, don’t drink your own Kool-Aid

This is all about the pitch. Of course it’s important to simultaneously hold in your mind all the truths about what you’re working on. Maybe you don’t actually have product market fit yet, or your marketing strategy. Perhaps your unit economics don’t yet work, or your team has major gaps. If you’re working on a new startup, likely, everything feels constantly broken, and everyone’s maybe going to quit.

You have to go and tackle all of those challenges with a clear mind — while simultaneously keeping a futuristic spirit that motivated people to join you on your journey.

It’s hard to be a product without a strong theory of distribution

Here’s a common startup situation. A team busts their ass for months building the first version of their product. It’s almost done. Now a big question emerges — how do you get the first people to use your product? Hmm…

If you find yourself at this moment, then you are already in a bad place.

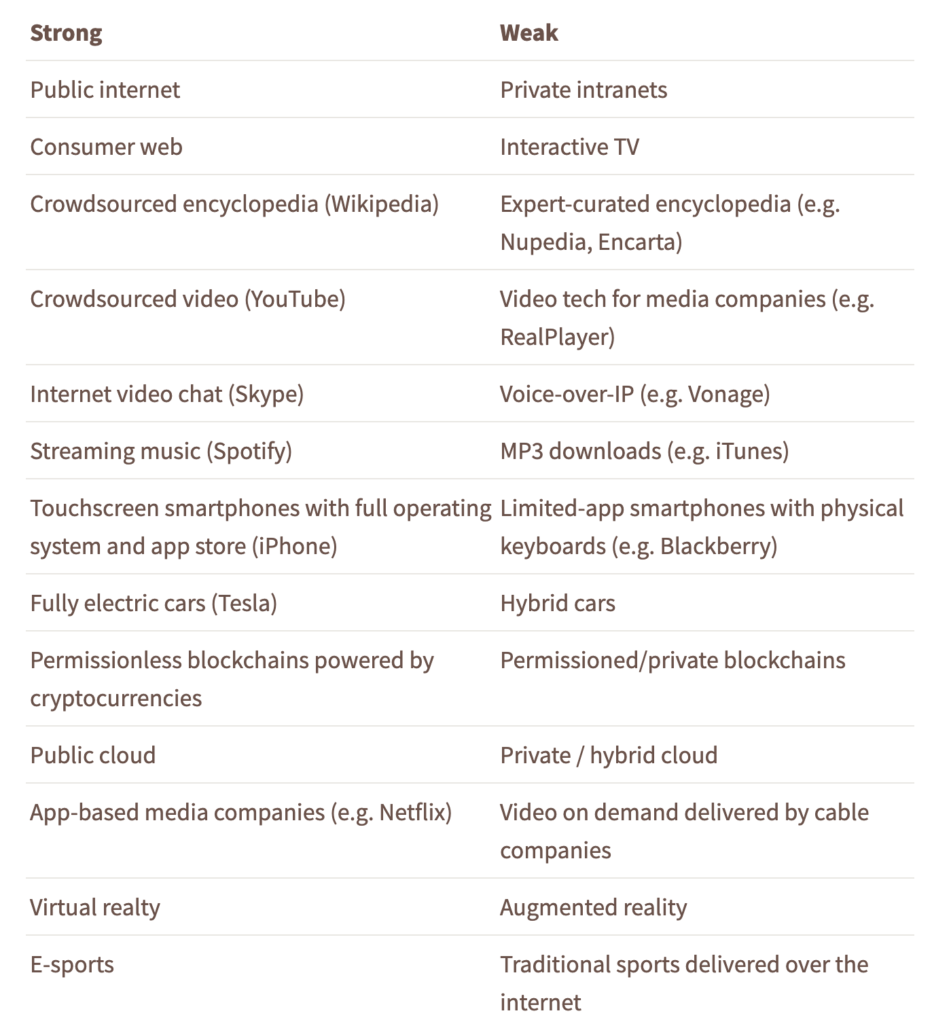

99% of startups are not differentiated on their underlying technology, and there is very little engineering risk involved. (I’m ignoring deep tech and foundational AI research companies, for the sake of this conversation). Because technology differentiation is no longer a real factor today start ups, it turns out that most products are succeeding or failing due to core product/market fit followed by the distribution strategy. There are over 9 million mobile apps. There are a billion websites. Figuring out distribution is key.

Dual insights needed

This is why I think startups end up needing both:

1) an insight about customers that gives them product/market fit

2) an insight about distribution that creates traction

People building products often have an easier time product/market fit because they are building for themselves, or a customer that they already know well. But the latter, about distribution, is often super difficult because once you onboard your friends and family, and look to expand the next set of hundreds of customers, you then dive into the world of growth marketing strategies and tactics which are its own very particular learned skill set.

The role of disruptive platforms

Sometimes when there’s a new breakthrough technology, as with what is happening in AI, or the Apple vision Pro, or Web3, it’s simply enough that the product has a “it works” feature. By simply being there on the scene when adoption of a new platform is happening, distribution happens automatically. I think that’s why we see that so many new great startups are launched right at the beginning of the platform.

But what happens when you are trying to launch the 9,000,001th mobile app? The first thing you do, naturally, is to try to read what’s out there. The other counterintuitive thing, is that although most of the knowledge in writing out there pertains to channels like SEO or paid marketing or influencer campaigns, many of these tactics best fit already successful products that have money and aim to accelerate growth. Many of these tactics simply won’t apply to you because they’ll be too expensive, or they will use mature marketing channels that just won’t be that effective. I often joke that by the time there’s a case study about a new marketing tactic or channel, the advantage has already been arbitrage away, and probably no longer works.

So what should you do instead?

Examples of products with natural distribution

Ideally the product and the distribution hypotheses happen at the same time, and reinforce each other. The Dropbox founders describe to me at the inception of their product, that sharing folders was part of the vision and was built in quite quickly. And later years this drove a significant amount of growth. Uber has natural virality because you often ride in a car with other people, or you ride a car to see somebody, and naturally you’ll mention the service. A product for creators, like Substack, will naturally encourage people on the platform to write and share content, attracting an audience who ultimately may also be writers themselves. Zoom, and other apps that help collaboration in the workplace, have natural features that cause you to bring in your coworkers as you use the product experience.

These are all examples of the best form of distribution, which are baked in to the product idea itself, rather than bolted on at the end.

The first set of users

Even once you have a basic theory for how your product will naturally distribute itself, you’ll still need to identify the first generation of users to help iron out all the issues, and give you feedback on whether your hypotheses were correct. In my years of studying new product launches, I can confidently say that the early years are often very idiosyncratic, and constantly changing. The reason for this of course is that marketing channels change all the time, but subscale ones that help you get your first couple thousand users, change even more so.

A few years ago you saw a trend were products would launch a huge conferences like SXSW. These days you see more effort on getting influencers involved early. Or “building in public” which makes yourself into an influencer. Several years ago many consumer products (like dating sites, new photo apps, etc) would launch on college campuses via the Greek system, because they were organized ways to reach thousands of undergraduate students. These days the organizations are often inundated with start up requests, and it’s become less effective. As a result all of these initial channels change all the time, and it’s up to the founders to figure out how to take advantage of what might work today.

The problem with these initial channels is that they eventually tap out.

The journey from channel to channel

Thus starts the journey of startups to grow and expand their portfolio of distribution channels, beginning with small and highly relevant ones, into the biggest channels.

I sometimes imagine a X Y axis, where X is volume of the channel, and Y is responsiveness. Early channels are often very low volume. But you want that. The reason is that they are highly relevant and they are small enough that larger companies do not focus on them. As I mentioned influencers are often an example of this, but so are niche newsletters, or or event marketing. However if you find this channel to be successful, you’ll also eventually one more scale. This involves you jumping onto the next set of channels, which will provide more volume but be much more competitive as a result.

Often times this is a period where you have one channel that kind of works, and you’re testing a few other channels simultaneously. Your efforts here should be experimental and iterative. You can often look at direct competitors as well as adjacent products and see what they’re doing, to inspire you on the right channel. The natural cadence of products will indicate to you the channels that are most likely to work. If you have episodic usage, you’ll probably need to do SEO/SEM, affiliate, or referral — something that helps you target high intent users. If you’re product is social or helps with workplace collaboration, then you might lean into referral programs and viral growth. Products in commerce naturally lead you towards paid ads, contact creators, etc. You can often learn a lot by talking to other people in your industry or an adjacent industries to see what works.

This is where sometimes I’ll see people working on episodic usage apps, like travel/health/etc asking the question, how do I make my product virally? I want free users! Of course the problem is, there’s a natural fit between a product and it’s distribution channels. Even though you might want free distribution, only very specific niches of networked products are able to grow freely. Generally everybody else must pay for their distribution, whether via referral or advertising.

Moving to volume-driven channels

Eventually you want to move on the XY axis towards volume. There are only about a dozen large scale distribution channels that can propel a product to scale. Advertising is on that list, SEO too, and so is viral growth. But these larger channels, by their nature, are both highly scaled but also have low responsiveness. As a result, you end up competing with some of the most famous brands in the industry as a result. Who wants to buy ads against the same audiences as major credit card or airlines? They have insanely high payback periods, and huge marketing budget, and are not that cost sensitive.

Ironically, this is where great products become to dominate. I started this discussion with the dual requirement of product/market fit, and distribution. But in the end, product/market fit actually dominates.

The reason is the following — the ability for a company to operate out in these most expensive and highly scaled channels comes from having a great product that generates a ton of word of mouth. More natural usage, the less marketing that has to be done. And the marketing costs that do exist end up being blended in with the large number of organic users.

The journey of a new product is to move, from unscaled and relevant, to highly scaled. And at the end, great products win.

Every time you ask the user click you lose half of them. (And this why tutorials, splash screens, and lengthy signup flows are a bad idea)

If you’ve been building apps for a long time and have seen the results of a lot of A/B tests, you quickly realize that people are a flighty bunch. Ask them to download an app and 80% will bounce right on that page. Ask them to sign up and 90% will hit the back button to avoid putting in their email and password. Ask people who’ve arrived from Google to read an article, to subscribe and get more updates, and 99% will head back to find the next article.

What happens when you ask for credit card and email

In the early days of Uber the only way to sign up was to give your email address a bunch of other fields and also your credit card number. Some of the big early winds in acquiring customers was just to make it so that you could sign up with a phone number and a password, and put in your credit card lead in the flow. If memory serves me right, these were increases on the order of +50%.

You get the drift of what I’m arguing.

So what happens when your designer has the fantastic idea of a stark and beautiful homepage for your new product that takes a few clicks to sign up, followed by a lengthy tutorial to explain all the features? Sometimes this becomes a life and death decision, because rather than signing up thousands of users into your private beta, which provides the traction to raise your next round of funding, instead only a few hundred make it through.

Streamline critical flows by minimizing steps

This is why, when I get feedback on a critical flow within a product, I always start by minimizing the number of clicks and steps. I asked whether each field in a sign-up form is really needed, or is optional. I ask the question of whether you need to user to do something now versus having them set it up in the future, when they’re more bought into the product. I ask to remove all the glitzy, visual steps that explain things and just ask the user to hit next. I move the sign-up form to the first experience, whether that’s on the homepage, or the opening screen of an app. If there’s a call action, while the user is doing something else, like reading an article, my theory is that you should be very upfront with it and make it a blocking modal, or not do it at all. No half measures.

The point of all, this, of course, is to get people into the magic of your product.

The magic is not in filling out forms or watching cute videos about your product, it’s about using your product as quickly as possible. As a result, the only acceptable forms of friction are ones that ultimately enhance the users ability to have a great experience. Thus product is much better experienced as an app, where you have a notifications channel and a richer experience, then, by all means, ask the user to download something. If a product is much better, when used with colleagues or friends, that it might make sense to take a lower conversion rate during the sign-up flow in exchange for some sharing or inviting functionality, that brings more people into the app. Ultimately, it’s all a trade-off, where every click drops off a huge number of users, so you need to spend that user intent very very well.

Add friction when it helps

Ironically, it can also be an anti-pattern to not ask users to sign up or install or do anything at all, because once they bounce, which they will inevitably, do, you have no way to get them back. That’s why it’s all a trade-off, and one of the trickiest things about the user growth discipline is knowing when to add friction, and when to take it away.

Also, interestingly enough, as you make it easier and easier to sign up to reduce friction the quality and intent of the users also decreases. If you double the number of sign-up typically, you do not get twice the number of paying customers.

Nevertheless it’s an important thing to remember: Every time you ask the user click you lose half of them. Be careful.

Above: Many small business figured out the hard way why coupon sites generate worse users

Incentive programs often don’t perform

The people you attract with referral programs, free trials, coupons, and gamification — folks who are “incentivized” as a broad umbrella category — are usually MUCH WORSE than organic ones. Worse LTVs, worse conversion, less engaged, and so on.

In a previous life, I headed up Uber’s $300m+/year referral program (“give $5 and get $5”) and learned a ton. Much of the learnings apply to the next wave of gamified consumer apps, web3 games, etc.

So why are these users worse? Let’s discuss.

When CAC/LTV spreadsheets fail

When a new product comes to market, usually the team will measure a baseline set of metrics around lifetime value, etc. if the numbers look good, they might say OK let’s roll out some incentives and get more users like this. Spreadsheets are built, budgets are planned, growth is forecasted, and the new growth project kicks off.

The problem is, all of these forms of incentives usually end up attracting a different type of marginal user that wouldn’t have signed up earlier. They are less qualified, more discount seeking, and behave differently. There is negative selection.

This is especially true when the product has been out there for a while and the core market has mostly been saturated. You also see significant amounts of fraud as users scheme to profit from the incentives. This could be a simple as creating a new account to grab an incentive or it could be something much more organized and nefarious.

This is why core metrics like LTV and engagement can often be half as good or lower, which is often enough to defeat the mathematics that justified the program in the first place. An additional user at upside down mechanics feels good from a top line basis, but in fact, fewer users would be better for the business model. And all the attention towards a complex referral program might take away attention from innovation elsewhere in the product.

One final issue that’s quite subtle, but very important: Cannibalization. You have an target market and sometimes it takes time for a product to spread through its ideal users — this is magical because word of mouth is free. And when it happens in an organic way, the intent is even higher. But if these ideal users encounter the product via an incentive program, you often “pull forward” these users, thus costing you money, when you would have gotten them anyway.

If this all sounds like I might have suffered some trauma from Uber, it’s because I did! Not only did the rider-side referral programs perform worse over time, and perform worse than other channels, in fact, the users were much worse than even users bought from paid ads. It was millions of dollars of spend that didn’t need to happen.

Why this matters — in the world of web3, gamified apps, etc

The ramifications of this are wide, especially on the world of web3, consumer apps that are gamified, etc.

First, it tells you that if you take a game or an app that does not have inherent engagement and retention, it is not enough to add gaming mechanics. If anything, the new mechanics might make things worse, not better, as they attract a group of users who respond to the mechanics, but wouldn’t otherwise use the underlying product. I think we saw a lot of this in web3, where incentivized attracted speculators early on, but struggled to find fun gameplay to attain actual users. Similarly gamified consumer apps (the trad kind) might attract and sustain a certain type of user who is happy to engage in any gamified app, and who will quickly move on because the underlying app doesn’t engage either.

Second, all of these dynamics create sort of a related dynamic to the Law of Shitty Clickthroughs. Not only do individual marketing channels degrade, but many of the new channels you add over time — because they are incentivized — perform worse than the initial channels. Thus the entire machine gets slower and harder as you go.

Final story on this from Uber, funny enough the referral program on the driver side attracted very positively selected users. Whereas the rider referral program got discount seekers, the drivers were highly money motivated. Because they were so motivated and signed up for larger referral bounties, they actually performed better after sign up. Even though referrals was 15% of sign-up they were well over 30% of first trips.

Incentives are a form of selection and you need to make sure you know what you’re selecting for.

Grand Theft Auto 6 and the future of AI

If you happened to miss it, a few weeks back, here is the game trailer for Grand Theft Auto 6. It’s worth watching, and is amazing on multiple levels. But GTA 6 might be the peak of the open world category, untouched by the next wave of tech, particularly generative AI.

Let’s start some facts: First, GTA has a reported budget of $1-2B, making it THE MOST EXPENSIVE GAME EVER

Not only is this the most expensive game ever, but compare it to movies. The most expensive movies, modern installments of the Star Wars and Avengers and Pirates franchises, clock in at a mere $300-450M. So this is nearly 5X:

I also think this is indicative of the pole position that gaming is taking in culture.

The recent trailer is now the most viewed non-music video on YouTube following 24 hours after its release, beating any movie trailer, TV show premier, and it topped MrBeast. In the first 10 hours, it hit 70M views, and at the time of this writing, a few weeks later, it’s at over 140M

It’s also funny to compare this to building a product in tech. Rather than “move fast and break things” instead this game:

took $1-2B to build, as we said

started dev in 2014, so it’ll be 11 years from start to release

1000s of developers, designers, etc crunching to finish

But as most of us in tech have been following, the tools and approach to games is rapidly changing.

How generative AI is changing the games industry

We are seeing generative AI hit multiple parts of game development. It’s early days, but there are quite a few places where this is hitting — this includes everything from concept art to assets within the game, to interactions with NPCs:

creating infinite varieties of concept art

designing/creating 3D assets

LLM powered NPCs

generating environments and worlds

synthesized speech for in-game characters

bots to play against, to onboard into PvP competitive games

endless quests, narrative stories, etc

etc

But that’s just the “weak form” innovations that are easily imagined today. The “weak form,” as my colleague Chris Dixon talks about, often comes alongside a strong form version, in a pair. The weak form is more easily understandable by the market, but it’s often the strong form that ultimately makes the bigger impact.

The “strong form” AI innovations will impact GTA in more emergent formats. To take a metaphor, it’s been cool to see modding allow for the emergent GTA RP (role play) community emerge, allowing for new game play as people play as cops, gang leaders, and other folks. Millions of people have tried this format of GTA, and even more millions have watched. It’s a new inventive form of play that didn’t previously exist.

I think the same thing will happen for future editions of the Open World genre. Yes, generative AI will be used to make games like GTA more cheaply ($1-2B is a lot!) or to get more content with the same dollars. But also AI will unlock new forms of gameplay as well.

I’m so excited, for example, about what happens with the GTA version of AI town — where NPCs have their own inner voices, motivations, and needs. You could imagine this underlying platform being able to power next gen social, dating, or otherwise. You could imagine thinking of open world games like GTA almost more like a physics engine, with a layer of modding and AI built in. And at some level, it’s a large enough playground that you can build a lot of other game genres inside of it (as Roblox does).

It’s just as likely gen AI will reinvent genres, not just make it cheaper to build

Think about what happened in the last content revolution, where user-generated platforms like YouTube and TikTok allowed video creators to dramatically reduce the cost of content. What creators used the technology for wasn’t to try and compete with Hollywood. People aren’t disrupting the 2 hour film or the 10 episode TV season with short videos. Instead, you see completely new video formats that are native to the medium, whether it’s personality-driven vlogging, video game streaming, long-form podcasts, or otherwise. These don’t compete with Hollywood — they take on entertainment by a wholly other approach, stitching together hours of entertainment 6 seconds at a time.

All this time we’ve been talking about big open world games, I actually think the best new experiences won’t resemble Grand Theft Auto at all. Instead, we’ll see new game genres that are rapidly released that compete in different ways:

Perhaps we’ll see games as a new format of meme. If a funny presidential debate moment happens between two candidates, perhaps later that evening you’ll see a fully-fledged fighting game (built in a no code, AI-enabled environment) become the huge hit later that evening

Perhaps gaming will be ultra-personalized, and people will make huge, immersive, deep games for their 50 person college club — just because they can

Perhaps gaming will be sold alongside commerce and other experiences. Today, you might build a huge gaming experience to accompany Harry Potter, but the economics don’t work to make it to promote your tiny Shopify store. If content creation costs fall close enough to zero, you might.

Either way, it’s really hard to imagine a big budget game like GTA happening the same way it is happening now. Instead, the content will be AI generated, along with the quest and maybe even the genre. And maybe it won’t look like what we consider a game today.

This last year has been a period of exploration for the games industry, but it’s still very early. Everyone is experimenting, which is a good start. And some tools, like Midjourney for concepting, has taken hold. But very little is actually in production. There’s a big transformation coming, and it’s going to be as big of a wave as anything we’ve seen in this industry.

As we enter a new year, many of us are setting goals to write more and create more content. As someone who has been writing consistently for the past decade, I wanted to share some strategies that have helped me in my writing journey, particularly in a professional context.

Collecting ideas

First and foremost, I emphasize the importance of collecting ideas. These ideas can come from anywhere – opinions, statements of fact, interesting factoids, statistics, or even visual content such as charts and graphs. These are things from X or books or Reddit or whatever.

I use an app called “Email Me” to quickly email myself these ideas and then compile them into a single note with a headline that inspires me to explore the topic further. So then my workflow is to open up this note with a bunch of bullets, each one a headline for a post, and then decide what to pick from

Let yourself write small

You should allow yourself to write things that are both big and small. But particularly, it’s great to give yourself permission to do much shorter pieces – tweets or LinkedIn posts – and they can even be a few lines. The frequency of creating helps you build the muscle for more later. Short helps you get over perfectionism, or a feeling of imposter syndrome, etc

The idea of “templates” is useful too – these are commonly repeating versions of posts that you can repeat, over and over, that always generate interesting content. Here’s some examples:

reviews of books

quotes from podcasts/articles

lessons learned from past projects

Q&A with a colleague/friend

top links about a particular topic

your answer about a particular topic

reflections on the past year/quarter

a factoid/statistic you found surprising

If you can collect these templates together, you’ll never feel writer’s block!

Setting aside time to brainstorm, and to write

Another strategy that has been effective for me is to have regular brainstorming sessions with a writing partner. This not only provides accountability but also helps in generating new and fresh ideas. At a16z we actually have a weekly content where people talk about what they’re working on each week, and riff on different concepts. It helps a lot.

Setting aside dedicated time for writing is also crucial. I find that scheduling 60 to 90 minutes, particularly in the morning when I’m fresh, helps me focus and eliminates distractions. I often do my writing Sunday afternoons as well, in prep for the week ahead, and try to crack out something that takes a few hours. These are my routines, and maybe you’ll find yours!

Distraction-free devices

I own a whole series of distraction free devices – I wrote my book on a dedicated laptop for writing that has nothing installed on it besides Ulysses, a writing app, and a browser. There’s some really cool Android tablets called BOOX that can pair with bluetooth keyboards – or you can use the Remarkable tablet that’s recently been out, with has a keyboard attachment. I also lock my phone into a plexiglass container with a timer to force myself to stay off my entertainment apps

In addition to these strategies, I’ve found that leveraging technology, such as using AI for brainstorming and voice-to-text apps, has been incredibly helpful in enhancing my writing process. I found chatGPT to be a strong brainstorming tool – just say something like, “I have X opinion, make a list of ideas that align, starting with Y and Z.” Then if you want more ideas, ask it for more. The hit rate sometimes isn’t great but you curate things down and then use that for your topic sentences for what you’re going to write. Voice-to-text is useful as well since it’s often easier to talk than it is to write. So if you ramble for 5-10 minutes there’s tools like Oasis AI that will clean it up into acceptable prose, which you can edit more later

Why “quality” is the enemy to writing

The top top obstacle to people writing/creating/building more (and this includes me!) is a misguided focus on “quality” as an excuse to procrastinate and to enable many other bad behaviors

Some thoughts:

1. quality focus hinders more writing and content creation

2. leads to procrastination and restricts experimenting with styles

3. taste develops faster than skills, causing disappointment

4. it’s important to accept failure as part of learning

5. start small, expand based on audience feedback

6. regular writing, experimenting with styles keeps process enjoyable

People often use quality as an excuse, thinking they need to craft a masterpiece to stand out online. They aim to produce only their finest work, expecting it to be widely recognized.

They say, look, there’s so much writing on the internet, and so much content. In order for my work to break out, what I need to do is I need to sit down and put down a masterpiece, something that will be recognized by people and I’m going to come up with the best ideas in the world.

I’m going to polish, polish, and polish. I’m going to put out only the best work. And then once that masterpiece is out there, then people are going to recognize it. Now, I would argue that that does not work at all. And the reason why that doesn’t work are really rooted in some really practical things.

Here’s why this approach is flawed

Firstly, focusing too much on quality is a great way to procrastinate. It leads to endless editing, turning what could be a quick tweet storm into a months-long essay project.

Secondly, it hampers your ability to experiment. When starting out, finding your voice is crucial, and it often takes time and trial and error. For instance, my own blogging and writing journey took about two years to find its stride. Experimentation is key, and a high-quality standard can stifle creativity and output. Initially, you might dislike your work as your taste develops faster than your skills, creating a frustrating gap between your taste and abilities.

It’s essential to embrace failure and learning. An over-focus on quality can prevent you from trying new things and accepting that some attempts might fail, setting unrealistic standards.

Increase the writing feedback loop

Instead, you should aim to increase your feedback loop. This means experimenting, seeing how your audience reacts, and evolving your content based on their responses. For example, start with a tweet, expand it into a thread if it’s well-received, and then develop it into an essay. This approach helps align your work with what your audience wants.

Good writing habits include writing regularly and giving yourself the freedom to experiment with different topics and styles. Discover what resonates with your audience and yourself. This way, you can build a diverse portfolio and find your unique voice or niche. It took years to figure out that people like when I write about charts and graphs

Remember, writing should be fun and conversational. Treat it as if you’re talking to friends. Don’t fret over a piece that doesn’t hit the mark; you can always try again. This philosophy of frequent, enjoyable content creation is what I’ve adopted in my creative process.

(above: Me in Sep 2023, a happy author, finding the Japanese translated version of my book at the wonderful Daikanyama Tsutaya Books in Tokyo)

Dear readers,

As many of you know, 2 years ago I published my first book THE COLD START PROBLEM. It aims to tell the story of why some products — YouTube, Instagram, Uber, Slack, Dropbox, and others — end up with hundreds of millions (and sometimes billions!) of users, and to provide the definitive theory of network effects which are often referenced in the tech industry, but only superficially understood. It’s been a success, now in a dozen markets, translated into many languages (including Japanese, Chinese, Spanish, Russian, etc).

Here’s a screenshot of some of the wonderful pictures that readers took during launch week:

This was an awesome experience. Nevertheless, I swear I will never write another book again . (I guess never say never, ha)

The creative process was a long, meandering path, and folks ping me from time to time because they want to take on a masochistic journey of their own. So this post will be about the messy, annoying, behind the scenes leading up to writing a book like this — it describes a bit the creative process, but also some of the major milestones and lessons learned.

Hopefully it will be useful for someone in the future who is thinking of a big writing project of their own.

A brief summary of what I’ll cover:

Month 0: At first, writing a book seems like a fun idea (until you figure out it’s not)

Month 1-6: Finding an agent, writing a proposal, and opening up your Christmas presents early

Month 6-12: Collecting and organizing the ideas — lots of fun chats, reconnecting with colleagues, talking to great people

Month 12: How to write the initial the outline, then the mega-outline — finding the formula

Month 12-24: The very messy middle, the trough of sorrow, the hard slog, followed by trench warfare (yes, it’s 3-5 years to write a book)

Month 24-36: Why you’ll feel insecure about the creative process

Final months: Just ship it already

I’m also going to link to various copies of intermediate content along the way — unfortunately I can’t share everything (like interview notes, etc) since some stuff will have to be confidential, but here’s a few interesting bits anyway

Mega outline. 30 pages that needed to be expanded to 300 pages

OK — so let’s get started on the journey.

Month 0: At first, writing a book seems like a fun idea (until you figure out it’s not)

I joined Andreessen Horowitz in mid-2018, I had already been writing on my blog for 10 years and I was kind of having some creative boredom over it. At that time, Elad Gil had just published his book and we had a nice convo at MKT’s lounge about a week after his book was out — he had amazing things to say about the process (he writes faster/better than me, in the back of Ubers it turns out), and he said it helped him a lot professionally. At a16z, as you all know, Ben and Scott have both written fantastic books as well, and it seemed to really be great for them professionally, so I thought it might be a fun challenge to do the same. So think of the motivation as 50% a creative challenge, and 50% seeing what it had done for other people.

I had two lines of thinking in terms of picking the book topic. First, I’ve had good luck taking ubiquitous jargon and writing the definitive blog post on the topic — something I did with growth hacking, CAC/LTV, viral loops, and concepts like that. I had a few ideas bouncing around in my head that felt like good candidates. “Power users” was one — a term we use willy nilly, but without a strong theoretic underpinning. “Network effects” was another, since we were talking about it at a16z all the time, but when it came time to look at the metrics and answer the question — OK so does this product have it!?? — then it got a little mushier. Another was “Product/market fit” or “MVP” and expanding those concepts much further.

The other line of thinking revolves around answering the big question — why? I decided my focus would be on something targeting a very small group of nerdy founders and executives, rather than a wide topic that might be more mainstream. I could write about, say, career advice or how to start a business (in a general sense), but felt like those would be too broad.

In the end, I picked the topic of network effects because it’s a genuinely important topic, I felt like I had something to say, and I also felt like it could fold in a lot of concepts from my prior work on growth. Once I started down the path of picking, I started to talk to people at a16z about it — they recommended I start with writing a book proposal.

Month 1-6: Finding an agent, writing a proposal, and opening up your Christmas presents early

The team at a16z was very helpful, and in the first few weeks I worked with Hanne Winarsky (now at Substack!) and others to start meeting agents, which is how I ultimately met Chris Parris-Lamb from Gernert who also represented Peter Thiel for Zero to One, and Pete Buttigieg for his book. I sent him the following book proposal with a placeholder name, MOONSHOT. The proposal usually kinda reads like a business plan:

Overview

Chapter summaries

The market

Author bio

Competitive books

We quickly agreed to work together, and that we would approach various publishers to solicit offers. The actual approach was kind of fun, honestly a more efficient version of what we do in venture capital. Chris ran the whole thing, and the process looked like the following:

Chris approached publishers and sent along the book proposal

They read the proposal (thank you!) and asked for 30 minutes of time

We got on the call and they asked me detailed questions, showing they had actually read the proposals — UNLIKE a typical startup/VC process where the founder uses the time to present

Later, they submitted an offer (I think 7 did?)

Chris then took the top half of the offers, and gave them a second chance to bid again

The top 2 bids were close, but I chose to work with Hollis Heimbouch at Harper Business

I chose Hollis because she’s legend in the industry, and worked with Jim Collins, Clay Christensen, Satya Nadella, and others on their most famous books — a16z had also worked with her for Ben’s previous book and it went well. My advance was high mid six figures, which I was told was very good for a first-time author, and would be paid out in parts as the book progressed (one part at signing, the next on the draft, the next at publishing, etc).

The entire process of doing this was maybe 3-4 months? I’ve described the early days of this as “opening up your Christmas gifts early” because you get all the good vibes up front of selling the book, without the work of actually writing anything. But soon I was going to pay the price!

Month 6-12: Collecting and organizing the ideas — lots of fun chats, reconnecting with colleagues, talking to great people

The rest of the first year was pretty fun as well — I realized I needed to do a lot of primary research, so I started reaching out to people I respected, asking them for short interviews. Thank you to Li Jin who tag teamed with me on many of these interviews, where I asked open-ended questions, heard stories, and tried to write as much of it down as possible.

Readers want to hear opinions. The sharper and funnier, the better, and I had a theory that if I could collect all of it, then that in itself could be the bones of a book. Thus, I wrote down pithy, opinionated statements whenever I heard them — anything that might be a good tweet would also be a good title or a good opening paragraph. Opinions like, “launching with Techcrunch is stupid” or “never build a social network, it’s just too hard” — those are gold.

All the interviews went into a spreadsheet tracker like this, which linked to individual notes for each, plus a little summary.

In the end, I ended up with 200+ interviews from people in the industry, and pages and pages of opinions and thoughts. It was absolute chaos. But I could also tell there was something interesting in there. I eventually interviewed some senior folks in the industry — the founders/CEOs of Slack, YouTube, Twitch, Tinder, Dropbox, Zoom, Linkedin, and may others — those all ended up being super fun, and were the showcase stories in the book. Getting time with these folks ended up being some of the most memorable moments while writing the book.

Month 12: How to write the initial the outline, then the mega-outline — finding the formula

If you have hundreds of pages of random notes from interviews, plus pages of research, and a jumble of ideas in your own head — what do you do? You need some kind of organizing principle that makes all these ideas readable. I figured there was probably a formula in some of the best business books out there, and so I re-read Lean Startup, Crossing the Chasm, Innovator’s Dilemma, and many others.

What you find it that the bones of the book often look something like this:

Opening story

Describe a big problem/dilemma/question

Present a framework

Go through one part of the framework

Start with an anecdote

Then describe the theory

Go through another part

Then another part

Then again…

Conclusion

This isn’t all business books, but look, it’s pretty ubiquitous. And so I thought I’d start by structuring my initial outline kind of like this, which is how I ended up with the following short version of the outline. The first book outline.

Btw, Ryan Holiday has a great discussion of how he wrote his book, with tons of photos, and I want to link that here. He has a photo of a box representing every topic/idea in this book, each one in a note card, categorized into sections:

I sort of ended up doing the digital version of this, where I created a document that I called my “Mega Outline” — where I took every opinion/point that I wanted to make in the book, and built out the first 2-3 levels of bullets in a much larger version.

Here’s the first page, so you can get a sense:

I’ve linked the entire Mega outline here if you want to peruse — it’s 30 pages where each page needed to probably be 10x’d. That is, 1 page of outline = 10 pages of written prose, which I quickly figured out as I began to write the first few chapters. There’s a funny George RR Martin discussion (he’s the Game of Thrones guy) where he talks about how some writers are Architects, and some are Gardeners. The architects do what Ryan Holiday and I both do — we have some chaos at the beginning, which we try to ruthlessly suppress, and use some organizing principles to put it together. Once there’s a structure, then that’s like a foundation of a building — the architects then write, floor by floor, and build the whole thing. Plus some polish at the end. It turns out that GRRM describes himself as the other archetype, the gardener, where you sort of plant some interesting points here and there, then revisit them as you write. But that’s why his books are amazing and take 10 years to write.

Month 12-24: The very messy middle, the trough of sorrow, the hard slog, followed by trench warfare (yes, it’s 3-5 years to write a book)

This whole middle section after the first year gives me PTSD so I won’t dwell too much on it, and just cover the lessons learned. The mechanics of this phase are pretty simple — you really just need to translate the mega outline bullet by bullet into pages of written prose. But here are all the problems you’ll face:

Your normal tools are not good for writing a book. Most writing that you do on a daily basis, like email, might be composed of a few paragraphs. That’s easy. If you need a longer document, then you might have multiple sections that contain multiple paragraphs each, and you’ll use Microsoft Word or GDocs. But what if you have a book with 7-10 parts that contain 5-10 chapters each, that contain 3-4 major sections that themselves contain a large number of paragraphs? And what if halfway through, you realize all the stuff you’re writing in one section should actually belong as a chapter in another section? Also what if you want to do a word count of different chapters or sections? It’s all a pain. In the end, I used Ulysses which at least has the concept of nested folders, and then each chapter would be a folder that would then contain files containing each part. The app then sync’d it all to a bunch of Markdown files in a Dropbox, so that I could work on it from multiple locations

You write on a computer, and your computer is very distracting. You need a browser to do research, but your browser is also where you can check what’s happening on social media. You can’t fully turn off the internet, since you need to do research. And sometimes you need to go to YouTube to watch an interview, but right next to the video you’re supposed to be watching is a gadget review for something you might want to to buy. So what do you do?

Distraction free devices and treating yourself like a kid. Eventually I started to try and buy a bunch of different tools to keep myself focused. I bought a plexiglass timer safe thing and I’d lock my personal phone away for an hour or two at a time. I bought a separate laptop, and put it in a different location, and turned on all the child-safe filters so that I couldn’t go to Reddit, Twitter, etc. If I needed to look up research, I would often just print out pages and pages of it, so that I would stay analog and not mess around. I bought a series of e-ink Android tablets called the BOOX that could run a Markdown editor, connect to Dropbox, and could pair a nice keyboard.

Say goodbye to vacations, weekends, and evening time. To hit the deadlines I had set for myself, I ended up converting a lot of my holidays and weekends into writing time. It’s hard to write for more than, 3-4 hours in a row, so you still can go somewhere nice and sunny — but I found that I needed to wake up, work out, and get writing before noon, in order to make progress. You get your evenings, but it’s tough. And weekends are like that too.

Here’s a funny photo of one of these kSafe timers I’d hide my phone into during my writing times — by the end, I had 5 (!!!) of these in various writing spots, so that if I was feeling in the mood I would throw my phone in:

I have to admit, it was a grind. Not easy at all. If there was a point where I could have gotten stuck and quit, this would have been it.

Month 24-36: Why you’ll feel insecure about the creative process

One of the craziest things about writing a book is that it’s such an incredibly solitary experience, and there’s eventually a point where you’ve written enough that you feel sorta okay about where it’s going, but no one else has seen it yet. And so it might suck. But you’re honestly not sure. I got got to this about 2 years into writing the book. I had written the first ~10 chapters (out of 35), and I had a lot of questions for myself:

Is this book any good?

Am I saying stuff people already know?

Or is this book too nerdy, and going into details that are unnecessary?

Are the stories actually interesting, or too obvious? Have people heard them already?

And to be honest, you kind of don’t know until you take a half completed version of the book and ask a few trusted friends to read it. I got a bunch of very very good feedback — thanks in particular to Lenny Rachitsky, Sachin Rekhi, and many folks at a16z for taking the first crack — and it was also the first time my publisher and agent were reading it. I got a bunch of useful conceptual feedback, for example that the first few chapters felt a little slow to get into the action. It felt too theoretical at parts. There were certain specific topics that felt trite. Some sections felt repetitive. And so on. Brutal honesty is what you need here. In the end I also felt like, underneath the scruff, was a book that I would really enjoy reading myself, and that it just needed to be tightened.

I will say, the most painful refactoring happening in this period. As I neared completion of rough versions of all the various chapters, I ended up with a roughly 100,000 word book (which is normal, turns out). Sometimes it takes 3-5 years to fully get to this, and the fact I had a demanding day job and was able to finish in ~3 years — that’s great. But if my worry was that if I had to significantly rewrite portions part way through, it would become a 5 years process, which I’ve learned is not uncommon. This kind of refactoring particularly comes when you have a full length book and then you decide to combine a chapter or two. Or to take a theme that’s appearing in a few spots, and make it into its own section. And then you have to update everything in the book so that it flows properly. It’s easiest to do with a blog post, or a document, or something like that, but with a 35 chapter book — that becomes a heavy lift. But so it goes.

Final months: Just ship it already

By the end of the writing process, I was dead tired. Honestly, I got to a point where I was both simultaneously feeling good about the materials, particularly the first few chapters that I had polished up. But also the process was long and arduous and I was ready to just ship it. The problem with books, however, is that they are really developed in a waterfall process for good reason — once you submit the book, and it’s printed, that’s that!

One fun back and forth happened as I started to work on picking the final cover. I worked with a designer who had done a lot of work on Stripe Press books, which I always loved — however, they are boutique operation which gives them a lot of latitude on what can be done, and the designs often had very small text on the cover (after all, the title will be somewhere on the web page in a digital-first experience, right?), or prescribed weird materials. It was a negotiation to figure out what was actually possible.

I also learned that almost all the US hardcover books are printed at one company (crazy???) and here’s an excerpt about that from a Vox article:

Most book printing happens in the US. Books with heavy color printing, like picture books, are sent to China, but in order to keep the cost of shipping low, most publishers do the rest of their printing domestically. That’s getting more and more difficult to manage.

Until 2018, there were three major printing presses in the US. Then one of them, the 125-year-old company Edwards Brothers Malloy, closed. The remaining big two, Quad and LSC, attempted to merge in 2020, but then the Justice Department filed an antitrust lawsuit. Quad responded by getting out of the book business entirely; LSC filed for bankruptcy and sold off a number of its presses. Smaller printers have continued to operate, but the infrastructure to keep up with the demand for printed books in North America is in shambles.

Crazy right? Couple other interesting things I learned at the end:

You only need ~10,000 preorders to be a bestseller — far below what it used to be

There are tons of books that become best-sellers because people buy many, many copies of their own books — often via anonymous networks of buyers to obscure what’s happening (I did not do this, btw)

The US is not actually the primary market for business books, at least by units — it’s China. There’s usually 3:1 ratio of books sold there versus the US

The average book has 250-500 books sold in its lifetime (!!!) — and maybe the median is more like a few thousand. But either way it’s quite low

Anyway, as the final months approached, I traded a bunch of revisions with Hollis and her team at Harper Business. Even though I was very tired at this point, I had the incredible help of Olivia Moore at a16z who did a once over at the end, that really polished things up, as well as my agent Chris, and many others. There are way too many people to thank, so I encourage you to look at the acknowledgements :)

It was only in the final months that I started to think about marketing the book. I also have a ton of notes there :) Will share more later. In the meantime, hopefully y’all found this interesting! It was a good 3+ years of my life and there’s finally enough distance to reflect now.

This is a small deviation from my usual topics, but wanted to share. This is one of the most important graphs that I saw in 2023 that has led to behavioral change for me. This is in Peter Attia’s book Outlive.

Here’s the graph:

tldr:

if you want to be able to briskly climb stairs when you are 75, you need to be in the top 95th percentile of cardiovascular fitness. Even at 95th percentile, it’ll be hard to jog up steep hills, etc — you’d have to be an elite athlete.

But if you are average/low, you may not even be able to do any of that. And it seems unlikely you’ll be avg/low now (I’m in my early 40s) and then somehow go from 50th percentile to 95th. So basically it’s better to get started

Thus, after reading his book, I reluctantly started running again even though I hate it. And am also doing some peloton / cycling outdoors when time/weather allows

I enjoyed his book, and I posted a bunch of my other book recommendations from the past year over here.

I was recently interviewed by the great Brian Balfour (CEO/cofounder of Reforge) and Fareed Mosavat (ex-Reforge/Slack/Zynga) which turned into a lively discussion — I think we could have gone longer! — which we just published in two parts. You can listen to both parts below, and the kind folks at Reforge also typed up some notes summarizing some of the major points made in the interview discussion.

2024 Predictions: the future of product, growth, and AI What’s in store for 2024? Andrew Chen, General Partner at Andreessen Horowitz, joined us on the Season Finale of Unsolicited Feedback to share his insights.

High Growth, high churn? Many AI experiences are currently seeing high growth and high churn due to their novelty factor. The question remains: can they sustain growth after the novelty wears off?

MVPs Have power, for now… AI is in the early stage of its S-curve, similar to the early days of the App Store. This period is characterized by rapid innovation and experimentation.

To Predict the future, look at the past The MVP strategy works well in the early stages of technology, but as it matures, the standards rise. The Apple approach of perfection might be the key in the long term.

More IPOs in 2024 Expectations of more IPOs in 2024 are high, given the maturation of businesses and the market’s readiness for fresh players.

More M&A in 2024 An increase in mergers and acquisitions is anticipated in the startup market, primarily involving startups themselves.

Big Breakthrough in AI in 2024? While major breakthroughs aren’t guaranteed, wider capabilities and integration of AI in everyday tools are expected.

More Product managers in 2024 The demand for product managers is predicted to rise as companies continue to grow and evolve.

The Law of shitty clickthroughs This law dictates that the performance of any marketing channel degrades over time due to increased usage and saturation.

If You’re reading about it, it’s probably too late By the time a marketing channel becomes mainstream, it’s often already fully utilized.

Phone Calls? don’t even get me started Over-saturation has led to the decline of channels like phone calls and SMS marketing.

The Running start Success in big channels requires initial momentum, typically from non-scalable, unique marketing approaches.

Defensible Growth channels often mean going niche Focusing on niche markets can help make growth channels more defensible and sustainable.

The Power of organic traction Organic traction is crucial for crossing over to higher volume channels and creating a loyal base.

Building a brand Developing a compelling narrative or brand is essential in overcoming the challenges of saturated channels.

Lessons from Gaming: the power of community, creativity, and storytelling The gaming industry offers insights into growth and product development, emphasizing community building, storytelling, and technology.

The Anti-MVP approach In gaming, extensive development and testing before launch are common, contrasting with the tech industry’s MVP approach.

Launching is a community effort Gaming studios excel at building anticipation and community engagement before a game’s launch.

The Intersection of culture and technology Gaming combines culture and technology, creating engaging experiences that resonate with players.

Storytelling is as important as technology Storytelling in gaming emphasizes the importance of narrative in product development and marketing.

Doing a short round up on various links, books, a quick life update, and other stuff going on. First, I did not write much in 2023 (I was busy!!) but am proud of what I published…

Blog posts from 2023